08 July 2026

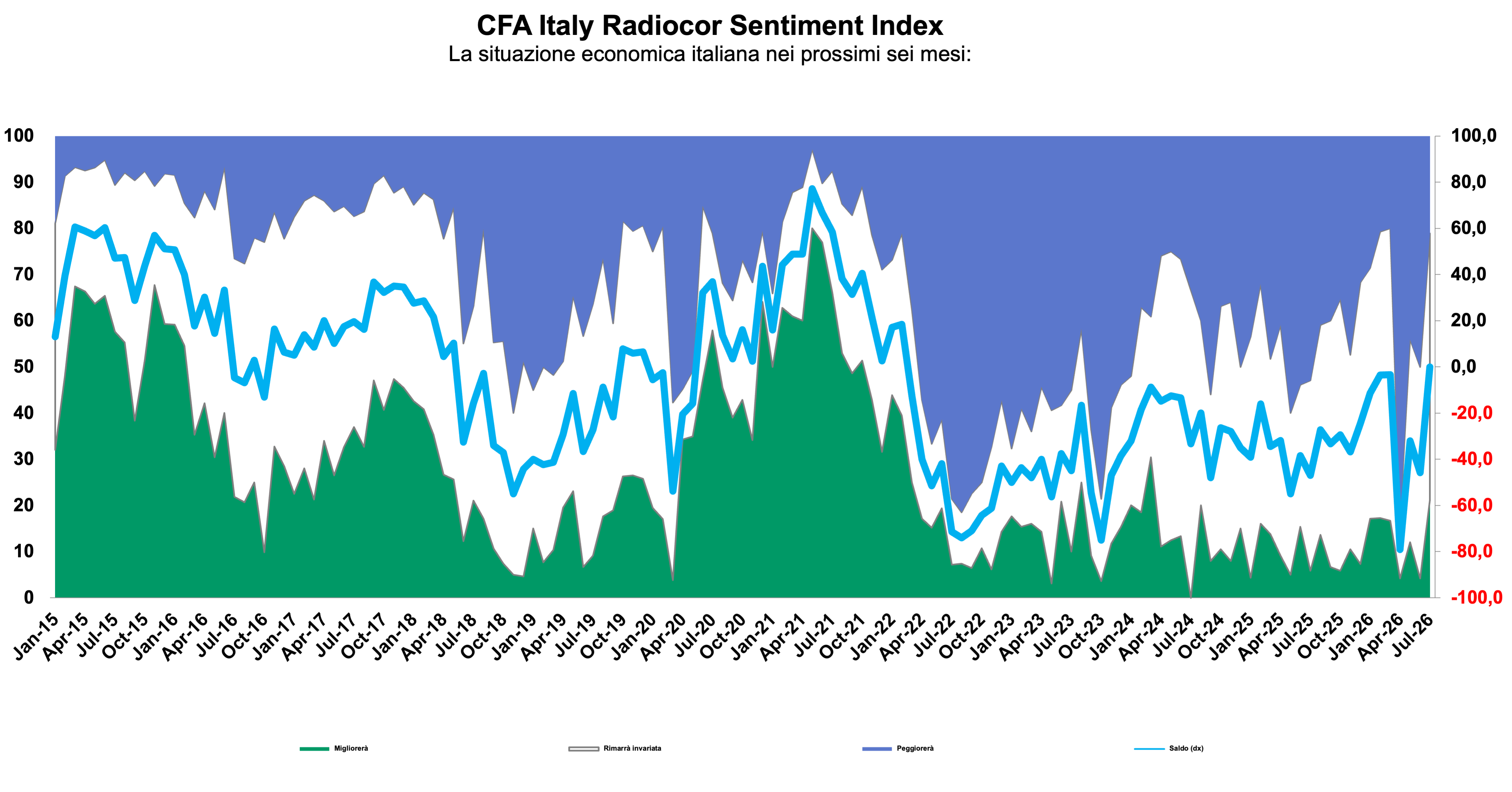

After months dominated by geopolitical uncertainty and concerns over global growth, confidence among Italian financial professionals has staged a significant recovery. The latest CFA Italy-Radiocor Sentiment Index, conducted between 19 and 30 June 2026 among members of CFA Society Italy in collaboration with Il Sole 24 Ore Radiocor, points to a marked improvement in market expectations, with the headline index returning to zero for the first time since February 2022.

The result marks a 45.8-point improvement compared with the previous survey and represents a symbolic turning point. Since early 2022, sentiment had remained consistently negative, reflecting first the economic consequences of the war in Ukraine, then the inflation shock and, more recently, the escalation of tensions in the Middle East. The latest survey suggests that, while uncertainty has by no means disappeared, market participants are beginning to look beyond the most adverse scenarios.

A shift from risk aversion to stabilisation

The rebound is particularly noteworthy given the backdrop against which it occurred. Only a few weeks earlier, the deterioration of the geopolitical situation involving Iran had fuelled concerns over higher energy prices and a renewed slowdown in global activity. Since then, investors’ assessment of the macroeconomic environment has become considerably more balanced.

Nearly eight out of ten respondents now describe the Italian economy as broadly stable. Expectations for the next six months reveal an equally balanced picture: 21.1% anticipate an improvement, the same proportion expects a deterioration, while 57.9% foresee broadly unchanged economic conditions. It is precisely this equilibrium between optimistic and pessimistic views that has brought the Sentiment Index back to neutral territory.

Europe regains momentum

The improvement extends beyond Italy. Expectations for the Eurozone have moved back into positive territory, with the sentiment balance reaching +5.3, suggesting that analysts increasingly expect the European economy to stabilise after a prolonged period of uncertainty.

The outlook for the United States remains more cautious, with the indicator standing at –5.3. Nevertheless, this also represents a significant recovery from the previous survey, indicating that fears of a sharp economic slowdown have moderated.

Inflation concerns continue to ease

One of the main drivers behind the improvement in sentiment is the changing outlook for inflation. After dominating investors’ concerns for much of the past two years, inflation expectations have become considerably more moderate.

For both Italy and the Eurozone, the balance of expectations has returned to zero, indicating an even split between respondents expecting inflation to rise and those anticipating further moderation over the coming six months. Although US inflation expectations remain somewhat higher, respondents also report a noticeable reduction in inflationary concerns compared with previous months.

This evolving outlook has been accompanied by more moderate expectations regarding future interest-rate increases, improving the overall environment for financial assets.

Italian equities lead the recovery

The renewed confidence is also reflected in equity market expectations. Respondents express their strongest optimism towards Italian equities, with sentiment reaching +21.1 for the FTSE MIB and +22.2 for the FTSE STAR. Expectations for the Euro Stoxx 50 are broadly neutral, while US equities continue to benefit from moderately positive sentiment.

At sector level, banks remain the preferred investment opportunity, posting a sentiment balance of +50, followed by insurance (+29.4) and utilities (+27.8). By contrast, respondents remain relatively cautious on sectors such as automotive, industrial machinery and construction.

Oil prices expected to normalise

The survey also points to a more constructive outlook for energy markets. After months of elevated volatility linked to geopolitical tensions, 52.9% of respondents now expect oil prices to decline over the next six months, compared with 23.5% who anticipate further increases. The resulting balance of –29.4 reflects expectations that the supply disruptions and geopolitical risk premium observed during the Iranian crisis will gradually recede during the second half of the year.

Overall, the July survey signals a meaningful shift in market psychology. While geopolitical risks and macroeconomic uncertainties remain part of the investment landscape, professional investors appear increasingly inclined to view recent shocks as manageable rather than systemic. The return of the CFA Italy-Radiocor Sentiment Index to neutral territory after more than four years of negative readings suggests that expectations have moved from crisis management towards cautious normalisation - i.e., a notable change in tone after one of the most challenging periods for financial markets in recent years.