30 March 2026

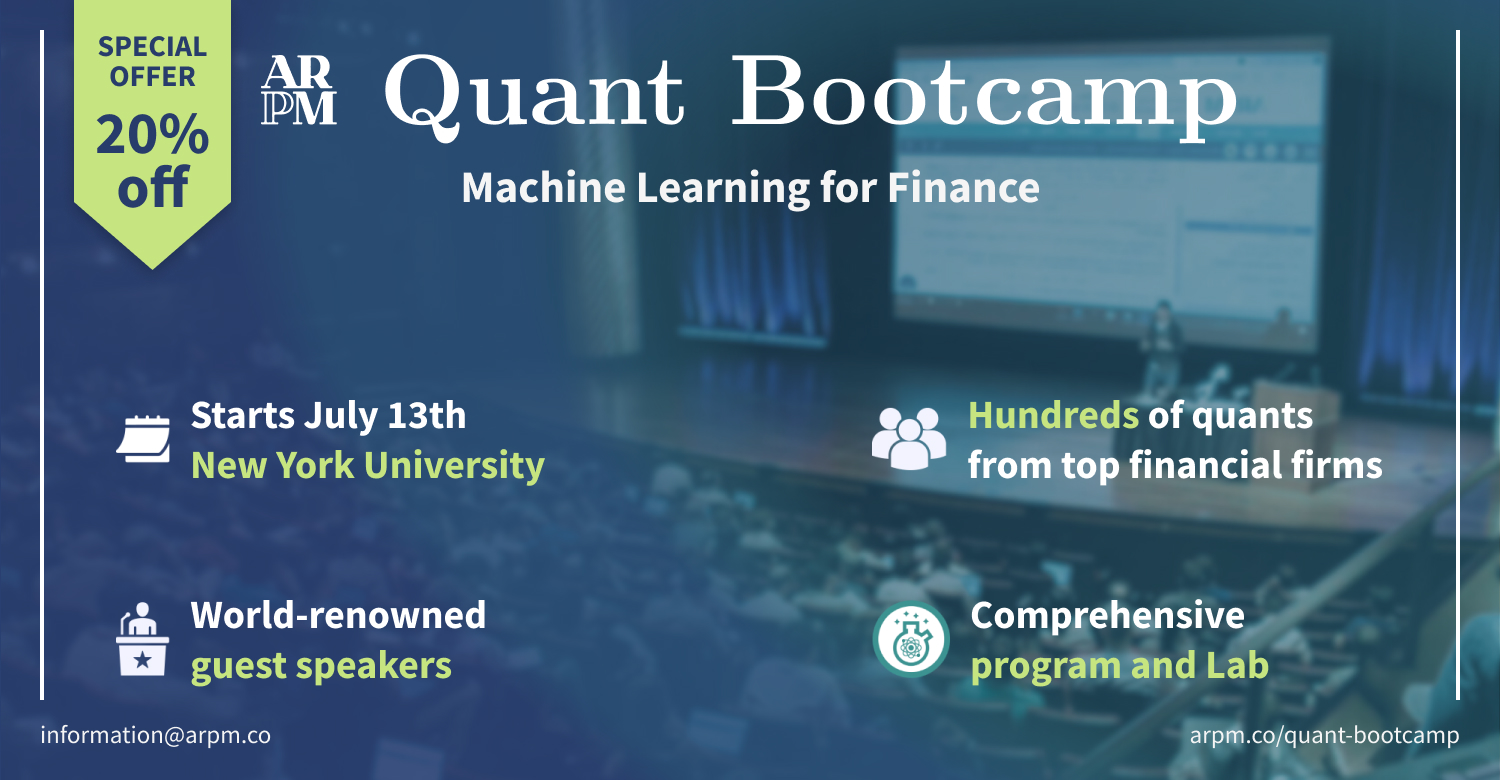

As machine learning continues to reshape the investment landscape, the ability to connect data science techniques with robust financial theory has become a critical skill for investment professionals. In this context, the Quant Bootcamp 2026, organized by Advanced Risk and Portfolio Management (ARPM), offers a structured and rigorous pathway to understanding how machine learning can be effectively applied within quantitative finance.

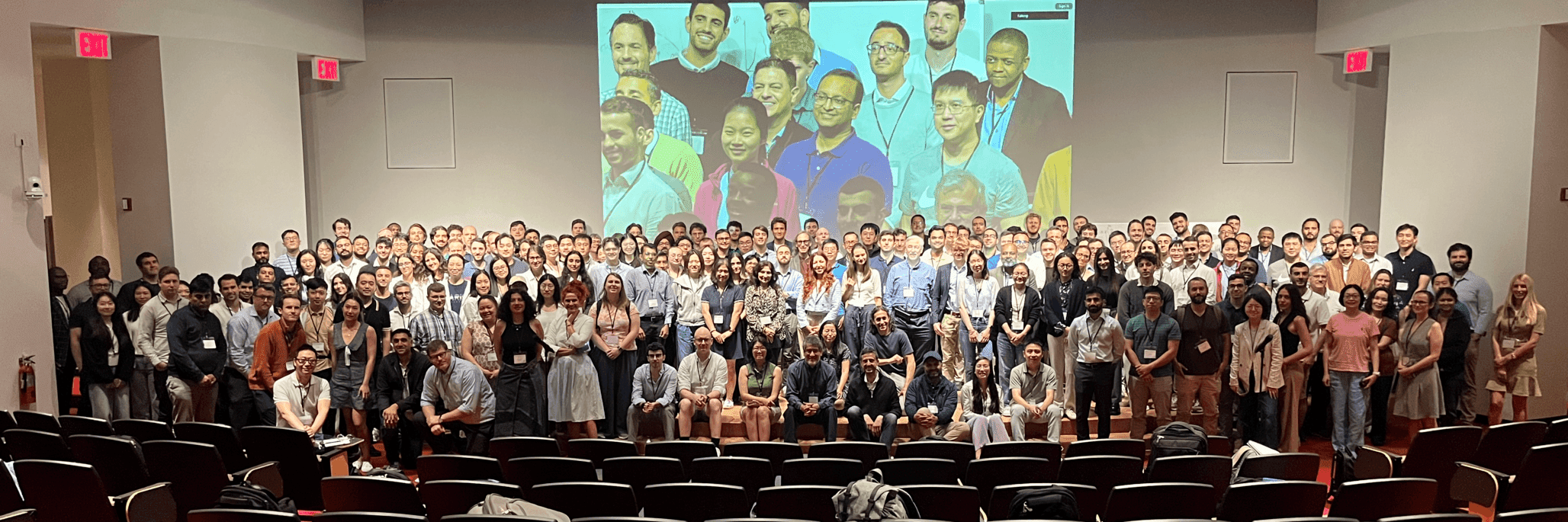

Now in its 19th edition, the program has established itself as a reference point within the global quantitative community, with more than 5,000 participants from over 20 countries. Unlike many initiatives driven by short-term technological trends, ARPM has built a consistent approach over nearly two decades, focusing on a unified mathematical framework that links machine learning to financial decision-making.

The bootcamp will take place in a hybrid format, combining in-person sessions at New York University from 13 to 16 July 2026 with online sessions on 23 and 24 July, allowing participants to benefit both from direct interaction and flexible access. The program is led by Attilio Meucci, founder of ARPM and a recognized authority in quantitative finance and risk management.

Over six intensive days, participants are guided from the foundations of machine learning to its practical applications in financial engineering, portfolio construction and risk management. The structure combines theoretical rigor with hands-on implementation, ensuring that concepts are not only understood but also applied in realistic financial contexts.

A distinctive feature of the program is its integration with the ARPM Lab ecosystem, which provides interactive materials, coding environments, case studies and even an AI-based learning assistant. This infrastructure allows participants to continue exploring and applying concepts beyond the classroom, reinforcing long-term learning and practical application.

The bootcamp also benefits from contributions by leading practitioners and academics, offering participants exposure to real-world perspectives and current industry challenges. This combination of academic depth and practical insight is one of the reasons why the program continues to attract a diverse audience of professionals, researchers and students.

For members of CFA Society Italy, the initiative represents an opportunity to strengthen technical capabilities in an area that is increasingly central to the investment profession. As quantitative methods and data-driven approaches become more embedded in portfolio management and risk analysis, programs such as the Quant Bootcamp provide a valuable bridge between theory and practice.

CFA Society Italy members can benefit from a 20% discount on the program by selecting the “Affiliate” profile and choosing “CFA Italy” during registration.

In a market environment where machine learning is often discussed in abstract or fragmented terms, the Quant Bootcamp stands out for its structured and coherent approach. By grounding innovation in a solid quantitative framework, it equips participants with the tools needed to navigate - and contribute to - the evolving intersection of data science and finance.